Short on time? Listen to a brief overview of this week’s review.

[soundcloud url=”http://api.soundcloud.com/tracks/335931234″ params=”color=ff5500&auto_play=false&hide_related=false&show_comments=true&show_user=true&show_reposts=false” width=”100%” height=”166″ iframe=”true” /]

What

- A debt fund that invests in deposits and PSU bonds

Why

- Superior returns to fixed deposits

- Low risk compared with category

Who

- Conservative investors looking for FD substitutes for 1-2 years

If your fixed deposits are maturing now, it is time to move to superior earning debt alternatives, given the sub-7 per cent bank interest rates. One such superior alternative is UTI Banking and PSU Debt Fund.

UTI Banking and PSU Debt Fund is a good alternative if you are looking for a liquid, low-risk, stable returning alternative to your FD, with at least a 1-2-year time-frame.

Fund and suitability

UTI Banking and PSU Debt invests in short-term bank deposits and short-to-medium-term public sector and government bonds. It generates income in two ways: One, the interest from these instruments provides accrual income. Two, the fund trades on the PSU bonds when there is a rally in their prices. This is typically possible when interest rate cuts happen. Although it trades in bonds, the fund’s volatility is much lower than dynamic bond fund categories as it keeps its average maturity low. As the fund invests only in PSU bonds, which are mostly AAA-rated, its credit risk also remains low.

The fund is suitable if you have an over one-year time frame and are looking at low-risk debt options. A 3-year holding period will fetch you capital gains indexation benefits and deliver better post-tax returns. Investments can be done in a lump sum.

Performance

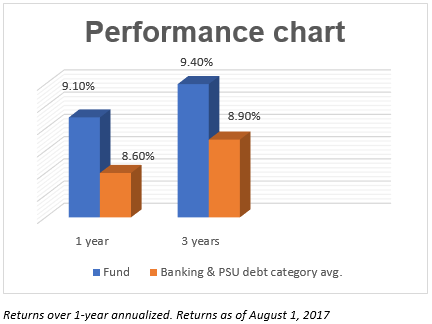

Banking and PSU debt funds are a relatively new category of short-term debt funds and do not, therefore, have a very long track record to go by. UTI Banking and PSU Debt was launched in January 2014 and has delivered returns of 9.4% in the last 3 years. ICICI Pru Banking and PSU Debt, a fund with a similar theme, is the only fund that has beaten UTI Banking and PSU Debt’s return over the above time frame. But the former’s performance has come with higher volatility.

For example, over the past 3 years, if one looks at rolling 1-month returns, UTI Banking and PSU Debt Fund has had negative 1-month returns just 1% of the time while ICICI Pru Banking and PSU Debt Fund has had negative returns 7% of the time. The volatility stems from the nature of instruments and maturity of papers. Higher maturity in the ICICI Pru fund has meant higher volatility and higher returns compared with the more stable performance from the UTI fund.

UTI Banking and PSU Debt’s minimum 1-year return thus far was 8.2%, among the best in the banking and PSU debt fund category, next to its peer fund from Reliance. This return is still higher than what deposits delivered in the last couple of years.

Portfolios

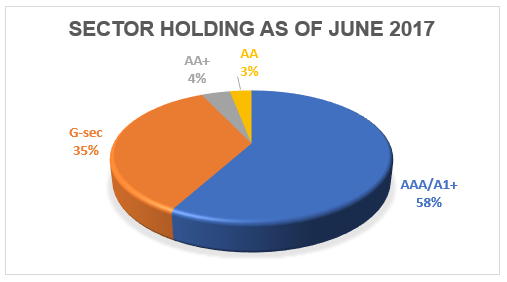

UTI Banking and PSU Debt has moved from holding bank deposits to more of PSU bonds. As interest rates fell, pure certificates of deposits lost their sheen and many funds in this category upped their PSU bond holding.

Axis Banking and PSU Debt though remains an exception in this category and continues to hold some proportion in deposits. That fund is therefore even lower on volatility and risk than the UTI fund. But in terms of returns, UTI Banking and PSU Debt scores higher.

UTI makes a fine balance between returns and an average maturity of holding. At 3.5 years, the average maturity of its portfolio is higher than the Axis fund (1.6 years) but lower than ICICI Pru Banking and PSU Debt (5.2 years). This essentially means it stands between the Axis fund and the ICICI fund in its risk-return profile.

UTI Banking and PSU Debt is managed by Sudhir Agarwal.

FundsIndia’s Research team has, to the best of its ability, taken into account various factors – both quantitative measures and qualitative assessments, in an unbiased manner, while choosing the fund(s) mentioned above. However, they carry unknown risks and uncertainties linked to broad markets, as well as analysts’ expectations about future events. They should not, therefore, be the sole basis for investment decisions. To know how to read our weekly fund reviews, please click here.

Wealth Conversations – April 2024

Wealth Conversations – April 2024- Temporary suspension of subscriptions in ” Mirae Asset Global Electric & Autonomous Vehicles ETFs Fund of Fund & Mirae Asset Global X Artificial Intelligence & Technology ETF Fund of Fund

- Merger Announcement: Aditya Birla Sun Life CRISIL IBX AAA Mar 2024 Index Fund

Here is everything that you need to know about Arbitrage Funds

Here is everything that you need to know about Arbitrage Funds- Temporary suspension of subscriptions in “DSP US Treasury Fund of Fund”

Hello Vidya Bala,

Great article about UTI Banking and PSU Debt Fund’s past performance. I wonder if, these funds are peaked at current 9.4% return. What do you see for the next 1,2 and 3 years ahead as far my investment into these debt funds? I feel it’s already too late and I feel I’m investing at higher share price, rather than low. Your advise is appreciated.

Thanks

-Raju

Hello Raju,

Sorry for the delayed reply. These funds will deliver FD-plus returns. The high returns we saw earlier was mostly from rally in bond prices as a result of rate fall. Even assuming we have a rate cut or 2 ahead, the returns may not be as high as in earlier years. This will be so with all debt funds. There is no such thing as low price or high price in funds. It is only the potential from here. Thanks, Vidya

Hello Vidya Bala,

Great article about UTI Banking and PSU Debt Fund’s past performance. I wonder if, these funds are peaked at current 9.4% return. What do you see for the next 1,2 and 3 years ahead as far my investment into these debt funds? I feel it’s already too late and I feel I’m investing at higher share price, rather than low. Your advise is appreciated.

Thanks

-Raju

Hello Raju,

Sorry for the delayed reply. These funds will deliver FD-plus returns. The high returns we saw earlier was mostly from rally in bond prices as a result of rate fall. Even assuming we have a rate cut or 2 ahead, the returns may not be as high as in earlier years. This will be so with all debt funds. There is no such thing as low price or high price in funds. It is only the potential from here. Thanks, Vidya

Hi, This fund crashed about 6% in last 1 week due to its exposure in ILFS sister concern.

1.What do you suggest , sell or continue to hold?

2.Since the bonds are supposed to be secure what happens to the customers who have sold right after the crash (those who have taken a hit and exited) and they recover a year later? do they pass on the benefit to the old customer?

Hello Sir,

Please contact your advisor on what you should do with your investments in this fund. Apart from the risk in the individual IL&FS group paper, the fund is seeing drastic erosion in AUM – this is in fact worsening the effect of the IL&FS paper. If the fund receives the payments in question at a later date, it will not flow to the earlier unitholders who exited the fund. It will accrue only to those who hold the fund at that time.

Thanks,

Bhavana

Hi, This fund crashed about 6% in last 1 week due to its exposure in ILFS sister concern.

1.What do you suggest , sell or continue to hold?

2.Since the bonds are supposed to be secure what happens to the customers who have sold right after the crash (those who have taken a hit and exited) and they recover a year later? do they pass on the benefit to the old customer?

Hello Sir,

Please contact your advisor on what you should do with your investments in this fund. Apart from the risk in the individual IL&FS group paper, the fund is seeing drastic erosion in AUM – this is in fact worsening the effect of the IL&FS paper. If the fund receives the payments in question at a later date, it will not flow to the earlier unitholders who exited the fund. It will accrue only to those who hold the fund at that time.

Thanks,

Bhavana