Important Lesson From The Past 6 Months

The past six months are a gentle reminder to the simple fact that…

Predicting the markets over the short run is extremely difficult. Period.

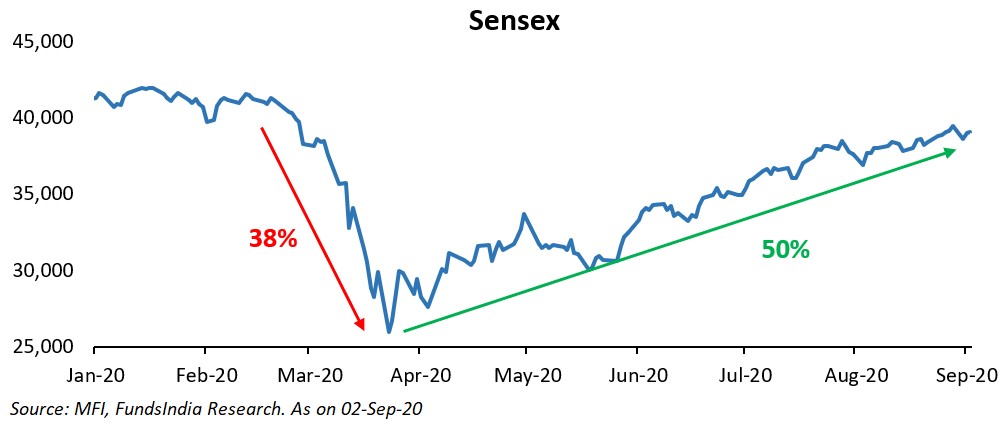

No one would have guessed at the beginning of the year, that an unknown virus from a small Chinese town would almost shut down the entire world and crash the equity markets by ~38%.

Similarly, no one would have guessed that in the middle of all this, when our Indian GDP was down 23.9% for the June quarter, the equity markets would recover a whopping 50% bringing it close to Pre-Covid levels.

We have always maintained our humble stance, that we don’t possess any special abilities to predict the equity markets over the short term.

Now that we acknowledge this, how do we go about managing your portfolios?

Simple. We PREPARE.

Ahem. Ahem. Sounds pretentious right?

Before you write us off, let me explain what ‘PREPARE’ really means when it comes to actual execution.

We boil it down to 3 important decisions that you should make at the current juncture.

Decision 1: Get Short Term Out Of The Way

It is extremely hard to think about the long term especially when we are worried about near term issues like our health, job, kids, family, money etc.

How do we get through this?

- Start building an Emergency Corpus (via safe high-quality debt funds) to cover 1 year of bare minimal expenses (this means no swiggy orders, amazon sales, netflix, etc.)

- No or Minimal Equity Allocation to portfolios built for near term goals (anything coming up in the next 5 years)

The basic idea is that, even if markets decline for some reason, you can comfortably reach all your near term goals without touching your long term portfolio.

In effect, you can provide the most important ingredient required for your portfolio to recover – ‘TIME’.

Once you take care of both your emergency corpus and short term goals (without depending on equities), your money anxiety hopefully should be much lower.

Decision 2: Revisit Your Risk Profile

Most of you would have answered the boring risk profile questionnaires at some point in time and figured out your risk profile. In fact, your portfolios would have also been built based on your risk profile.

When it comes to risk profile questionnaires, I often get reminded of an insightful Yogi Berra quote.

The last 8 months, though painful, provides us a great opportunity to find out our real risk tolerance.

Here is a simple practical approach to figure this out…

Quick Test 1:

What did you do in Feb-Mar 2020 when the equity markets fell by ~38%?

- Sold Equities: Implies low-risk tolerance

- Held steady: Implies moderate-risk tolerance

- Bought more: Implies high-risk tolerance

- Bought more and hoped for further declines: Implies very-high-risk tolerance

Does this match with your original risk tolerance?

If no and it turns out that you panicked and sold during the fall, it means your equity allocation was way higher compared to your ability to tolerate volatility (read as sharp temporary declines).

So this is a good time to gradually reduce your equity exposure and bring it to levels that match your risk tolerance.

If you have not sold and your risk profile matches your current asset allocation, your original asset allocation was right, to begin with.

You can continue with your original asset allocation. That is you don’t need to underweight or overweight equities. For a 50% equity allocation, simply stick to 50% and don’t make it 40% or 60%.

Quick Test 2:

Assuming the market falls from here for some reason, would you be willing to tolerate a temporary decline of say 20%* in your equity portfolio in the next six months?

For example, let us assume you have a Rs 50 lakh portfolio split equally between Equity (Rs 25 lakhs) and Debt (Rs 25 lakhs). 20% of the Equity value of Rs 25 lakhs, works out to be Rs 5 lakhs.

Would you be willing to tolerate ~Rs 5 lakhs temporary decline in your overall portfolio value in the next 6 months?

If yes, then your current equity allocation is right for you and you can continue with it.

If no and you are willing to tolerate declines but to a much smaller extent, then you need to immediately revisit your equity allocation and gradually bring it down.

Remember that if you reduce your equity allocation you also need to be ok with lower returns over the long term. It’s a simple trade-off. More the near term pain you can take more the long term gain. There is no right or wrong allocation. The ideal allocation is a portfolio designed to let you sleep in peace.

*While there is no hard and fast rule that markets should not decline more than 20%, going by the march decline which is around 25% lower from current levels and assuming slightly higher levels (given the surplus global liquidity), 20% can be a reasonable worst-case scenario to work with.

Decision 3: Prepare & Plan for different outcomes

Now that we are done with the short term and have revisited our asset allocation to match our real risk profile, this leaves us with preparing for different market outcomes.

1. WHAT-IF-THINGS-GO-WRONG plan?

While we have no idea what the markets will do over the short term, we always want to be prepared to make use of the opportunity if the market falls.

So a clearly defined plan helps us execute it during a fall without panicking.

Here is how the plan* looks:

If Sensex Falls to 32,000 – Deploy 30% of the money into equities

If Sensex Falls to 30,000 – Deploy 40% of the money into equities

If Sensex Falls to 28,000 – Deploy 30% of the money into equities

*This is a rough plan and can be adapted to individual needs

For eg: In the Rs 50 lakh portfolio that is equally split 50% into equities (Rs 25 lakhs) and 50% in debt (Rs 25 lakhs) let us see how this works.

Assume you have earmarked 10 lakhs of debt portion to make use of market falls –

If Sensex Falls to 32,000 – Deploy 3 lakhs into equities

If Sensex Falls to 30,000 – Deploy 4 lakhs into equities

If Sensex Falls to 28,000 – Deploy 3 lakhs into equities

2. WHAT-IF-THE-RALLY-CONTINUES Plan?

This is a good thing as our equity allocation will continue to do well. In this case, we will continue to monitor the equity markets for valuations and earnings growth. If at some point in time valuations become extreme (indicated via MCAP/GDP, PB, PE, Earnings Yield vs 10Y GSec) we might look at reducing equity allocations. At the current juncture, we continue to maintain a neutral view and recommend sticking to your original asset allocation.

3. Getting Overly Worried about a Correction? Sin a Little…

We have always warned you about the perils of market timing (trying to move in and out of equities) and the fact that there is no evidence of anyone consistently getting the market timing right.

However, after seeing the sharp market rally, you might have this sudden urge to sell some portion of equities. No worries, welcome to the rest of us.

This is precisely why we always emphasize on an evidence-based-process-oriented approach over emotional investing. So tempting as it may be, stick to your asset allocation as per plan!

That being said, at the end of the day as humans, we all have certain behavioral quirks that are difficult to get over with. Otherwise, we would have a world with only fit, super disciplined, super-productive people.

As with most things in life, the trick is to ‘strike a balance’ and ‘sin a little’… IF REQUIRED

If you find it difficult to stick to your investment plan, don’t give up on it completely. Instead of reducing equity allocation and shifting to debt, take a mid-path solution by moving into Dynamic Asset Allocation Funds.

The biggest issue with moving a portion out of equities is how to get back in. A lot of investors get it wrong and stay out too late as the markets always move ahead of the economy (remember what happened in the recent rally).

Dynamic Asset Allocation Funds can address this issue as these funds automatically adjust their equity allocation (reduce or increase) based on market valuations.

So if you find yourself getting too anxious or confused about the equity markets, you can start moving a small portion – say 10-20% of your equity allocation into Dynamic Asset Allocation funds such as ICICI Prudential Balanced Advantage Fund, Kotak Balanced Advantage Fund etc.

To reiterate, in our view, sticking to your original asset allocation will always remain the best solution.

However, worst case if you are not able to get over the anxiety and uncertainty regarding equity markets and have this urge to reduce equities, the mid-path solution of using Dynamic Asset Allocation Funds can be a good alternative though it means sinning a little.

This thought process can be summed up in our belief that,

An above-average investment plan that you can stick to is far better than a perfect investment plan that you give up on.

Summing it up:

While the temptation to time the market (read as moving out) is pretty high at the current juncture, long term investment success finally boils down to simple and boring activities such as being patient, staying disciplined, and sticking to the long term plan.

In line with our approach of favoring “Preparation” over “Prediction”, here are the 3 decisions that you need to make now:

- Get Short Term Out of the Way

- Revisit your Risk Profile

- Prepare and Plan for Different Outcomes

Think through these 3 decisions and make sure that your investment plan is the right one for you.

Happy Investing as always 🙂

Wealth Conversations – April 2024

Wealth Conversations – April 2024- Temporary suspension of subscriptions in ” Mirae Asset Global Electric & Autonomous Vehicles ETFs Fund of Fund & Mirae Asset Global X Artificial Intelligence & Technology ETF Fund of Fund

- Merger Announcement: Aditya Birla Sun Life CRISIL IBX AAA Mar 2024 Index Fund

Here is everything that you need to know about Arbitrage Funds

Here is everything that you need to know about Arbitrage Funds- Temporary suspension of subscriptions in “DSP US Treasury Fund of Fund”