If the below data has weakened your faith and interest in equity, then it could be a good thing!

‘The safest and most potentially profitable thing is to buy something when no one likes it’ said Howard Marks, one of America’s more successful investor. If you are not liking what you are seeing below, then you know Howard Marks’ wisdom should be your strategy for equity in 2017.

But what you buy and how you buy would truly matter and this article will seek to address that after letting you know what to expect in 2017.

| Indices | 2016 | 2015 |

|---|---|---|

| Sensex | 2.60% | -5.00% |

| Nifty 50 | 3.70% | -4.10% |

| S&P BSE 100 | 4.20% | -3.20% |

| S&P BSE 500 | 4.30% | -0.80% |

| S&P BSE Midcap | 8.50% | 7.40% |

| S&P BSE Small cap | 2.30% | 6.80% |

| Returns for calendar years. | ||

Equity markets to be volatile

We believe the equity markets could be volatile for a good part of 2017 because of the following near-to-medium-term risks, all of which are a spill-over effect of what went on in 2016.

- Impact of demonetisation on money supply and economic growth

- Impact of GST; the pain from which would kick in well into the year as its implementation has been postponed to June from April

- Impact of any higher-than expected rise in crude and commodity prices on commodity users

- Impact of US Fed rate hikes, if they come in quick succession

To add to these, there are too many global factors at play. These include elections due in multiple nations, including powerhouses France and Germany across Europe, Brexit being implemented, and policies of the new US government, and the rate and extent to which the US Fed hikes rates. The exact outcome and impact of what is yet to happen is best left out at this stage. What holds is that these have been, and will be, continuously evolving scenarios, impacting either corporate earnings growth or FII flows. In other words, you can expect bouts of volatility through the year.

What will keep the market going

Among the various events that will unfold in 2017, Indian markets will be clued on the following:

- Budget announcements

- Rate cuts

- Corporate earnings growth

While there may be much talk of a fiscal stimulus through the budget, we believe both rate cut and government spending (monetary and fiscal policy) must go hand in hand to tackle not only the pressure of a slowdown from demonetisation but also the unwillingness of companies to borrow and build.

We are not going to get into more details of these macros at play. What matters to us is earnings, stock market valuations and what can deliver in this scenario. Let’s dive into this.

Why there is upside yet

Despite two years of flat returns, the markets are at a price earnings ratio of around 20 times trailing (22 for the Nifty) and at 16 times on a forward basis (2017-18), considered to be trading marginally at a premium. If that be the case, where are the returns to be had? Where would fund managers go, to pick good stocks for you?

Let us take a broader index like MSCI India (which represents 85% of the India listed equity universe) to take stock of the valuations and returns of the sectors.

| Sector | Returns | PE | ||||

|---|---|---|---|---|---|---|

| 2016 | 2015 | 2014 | Dec-16 | Dec-15 | Dec-14 | |

| Consumer discretionary | 5% | -7% | 31% | 20.4 | 23.7 | 15 |

| Consumer staples | -5% | 3% | 20% | 35.4 | 38.9 | 44 |

| Energy | 5% | 0% | 7% | 13.2 | 12.8 | 11.1 |

| Financials | -4% | -5% | 47% | 16.0 | 15.2 | 17.5 |

| Healthcare | -15% | 7% | 42% | 26.0 | 36.8 | 28.7 |

| Industrials | 0% | -12% | 43% | 30.2 | 30.2 | 26.4 |

| Tech | -9% | 4% | 15% | 16.4 | 19.7 | 19.7 |

| Materials | 33% | -21% | -8% | 48.3 | -58.6 | 16.1 |

| Telecom | -27% | -4% | -8% | 19.2 | 23.7 | 28.4 |

| Utilities | 11% | -10% | 13% | 15.0 | 15.7 | 13.1 |

| Source: MSCI, Morgan Stanley Research | ||||||

The above table will tell you the returns delivered by respective sectors and their price earnings ratio at different points in time. Now, the point to note here is that the sectors that are now reasonably valued are not only the ones that account for a chunk of the index, but also account for a chunk of the profits of the index. In other words, there is still potential in the broad markets from ‘value’ sectors. And a few triggers could move these value sectors around:

- While the banking clean-up may get lengthened a bit if there are demonetisation-related defaults, it could well be offset by better financial strength and financial turnaround commodity companies (especially steel) that were large defaulters earlier. High CASA coming from demonetisation would likely take care of any further pain in the space

- The energy space has already been boosted post the recent decision of OPEC and certain non-OPEC countries to cut back on crude oil production. Both upstream and downstream companies can be expected to benefit from this

- Power utilities, especially regulated ones have better standing in a slowdown as their cost-plus model and assured returns provide earnings stability

- Commodity plays could also benefit from any recovery in global demand coupled with a supply shortage developing in the non-ferrous metal space

- The high sentiments in the US if translated into meaningful spending, could well lift sentiments for the IT space and current modest valuations could help

Given the low base of earnings for these sectors in the year gone by and that they account for a chunk of the earnings of the bellwether indices, a modest increase in earnings could deliver returns for the index.

We expect this is where fund managers would try and pick their stocks. But this does not mean the other sectors would not provide opportunities. For instance, the correction in consumer stocks as well as pharma could well provide select stock opportunities.

Hence, even if markets do remain volatile, it may be too pessimistic to assume that the market no longer offers opportunities.

Where to invest in equity

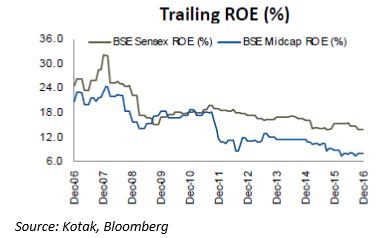

As an investor, we think investing a higher proportion in large-cap and multi-cap/diversified funds will yield better than going behind midcaps. For one, the trailing valuation of midcaps (Nifty Free Float Midcap 100) at close to 30 times is overheated compared with the large-cap space (Nifty at 22 times). Two, many of the sectors with potential that we discussed above have better quality companies in the large-cap space and in any turnaround, the larger companies get to reap the benefits first. Three, the below chart will tell you that the return on equity in the large-cap space is far superior and deserves better valuations compared with midcaps.

We will, over the course of the next few months, come out with calls on funds that are well-positioned to make the best of the opportunities in 2017.

Diversify your debt holding

For those invested in duration funds such as dynamic bond funds, it would have been a super-yielding 2016. The rate cuts and ensuing bond rally ensured double-digit gains. While those investing afresh may still have money to be made in this space, we would suggest addition of accrual funds besides dynamic bond funds.

Why do we say this? For one, the returns from duration is over for a good part, although you can expect it to comfortably beat the FD returns over the next few years. Two, while rates cuts may have to come about, when and how calibrated they are would depend on economic growth numbers as well as the Fed rate hikes. Three, there is already a significant pull out in the gilt space by FPIs who have been booking profits earlier. Fresh money from their end may reduce as the Fed rate hikes will reduce the spread between the two nations’ bonds.

On the other hand, there is still plenty of opportunity on the corporate bond space, where marginally higher yields do not necessarily come with high risk. Adding short-term debt funds (2 years) or income funds (at least 2-3 years) or quality credit opportunity funds (at least 3 years) if you have risk appetite for the last, would be a necessary diversification when you add duration funds.

Holders of bank deposits that mature this year, would have little choice but to go for debt funds to ensure that they do not suffer from reinvestment risks.

Asset allocation necessary

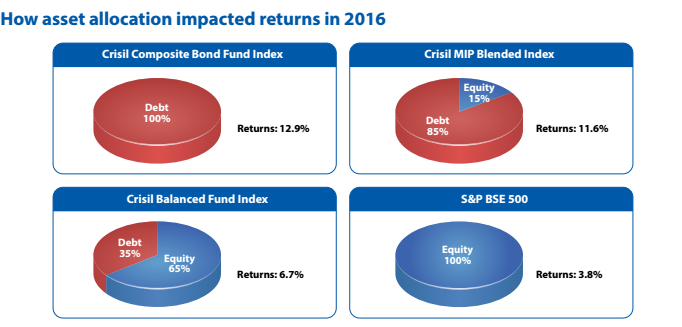

2016 illustrated quite well the benefit of asset allocation (see graph). We believe such allocation, based on your time frame and risk profile would be a necessity to shock-proof your portfolio. While the below returns should not be expected from debt in 2017, holding debt will certainly reduce your portfolio volatility while allowing you to participate in the debt rally that still holds steam.

FundsIndia’s Research team has, to the best of its ability, taken into account various factors – both quantitative measures and qualitative assessments, in an unbiased manner, while choosing the fund(s) mentioned above. However, they carry unknown risks and uncertainties linked to broad markets, as well as analysts’ expectations about future events. They should not, therefore, be the sole basis of investment decisions. To know how to read our weekly fund reviews, please click here.

Wealth Conversations – April 2024

Wealth Conversations – April 2024- Temporary suspension of subscriptions in ” Mirae Asset Global Electric & Autonomous Vehicles ETFs Fund of Fund & Mirae Asset Global X Artificial Intelligence & Technology ETF Fund of Fund

- Merger Announcement: Aditya Birla Sun Life CRISIL IBX AAA Mar 2024 Index Fund

Here is everything that you need to know about Arbitrage Funds

Here is everything that you need to know about Arbitrage Funds- Temporary suspension of subscriptions in “DSP US Treasury Fund of Fund”

Will equity LTCG be taxed in 2017 onward?

LTCG on equity (held for more than 1 year) continues to be exempt. On debt, LTCG (holding of more than 3 years) continues to get indexation benefits.

Will equity LTCG be taxed in 2017 onward?

LTCG on equity (held for more than 1 year) continues to be exempt. On debt, LTCG (holding of more than 3 years) continues to get indexation benefits.